报告地点:舜耕校区4号楼511会议室

报告时间:2025年7月4日(星期五)14:00—17:00

主办单位:山东财经大学统计与数学学院

协办单位:科研处,黄河流域生态统计协同创新中心,现代统计交叉科学重点实验室,统计学博士后科研流动站

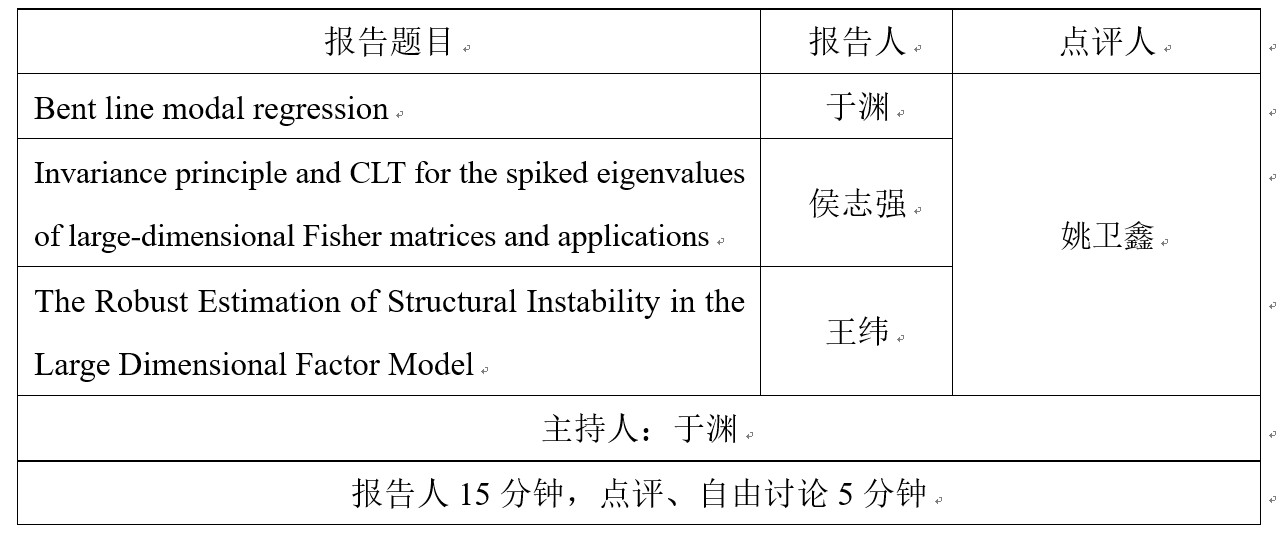

一、青年教师工作论文报告

二、特邀专家报告

报告题目:New Regression Model: Modal Regression

报告人:姚卫鑫,教授,美国加州大学河滨分校统计系

报告人简介:姚卫鑫是美国加州大学河滨分校统计系教授。他于2002年在中国科学技术大学获得统计学学士学位,并于2007年在宾夕法尼亚州立大学获得统计学博士学位。他的主要研究领域包括混合模型、非参数和半参数建模、稳健数据分析,众数回归,和高维数据建模。至今,姚博士已经发表了100多篇国际论文,还出版了一本专著。他担任过多个国际知名统计期刊的副主编包括Biometrics, Journal of Computational and Graphical Statistics, Journal of Multivariate Analysis, and The American Statistician。2020-2021年受邀担任Advances in Data Analysis and Classification的客座主编。姚教授是美国统计协会会士和国际统计学会当选会员。

摘要:Built on the ideas of mean and quantile, mean regression and quantile regression are extensively investigated and popularly used to model the relationship between a dependent variable Y and covariates x. However, the research about the regression model built on the mode is rather limited. In this talk, we propose a new regression tool, named modal regression, that aims to find the most probable conditional value (mode) of a dependent variable Y given covariates x rather than the mean that is used by the traditional mean regression. The modal regression can reveal new interesting data structure that is possibly missed by the conditional mean or quantiles. In addition, modal regression is resistant to outliers and heavy-tailed data, and can provide shorter prediction intervals when the data are skewed. Furthermore, unlike traditional mean regression, the modal regression can be directly applied to the truncated data. Modal regression could be a potentially very useful regression tool that can complement the traditional mean and quantile regressions.